The Age Pension is scheduled to be increased in 2026 in Australia and this will provide much relief to the ageing population who are experiencing an increase in the cost of living. Even though the government determines the specific amounts and indexation dates, the main goal of keeping the basic standards of living of retirees is to ensure a consistent ongoing increase in indexation of benefits according to the inflation and wage pace. This guide is aimed at explaining the general way that the new rates are usually determined, what you should expect with a regular increase and the eligibility rules in such a way as to be able to make your plans with confidence.

As anyone nears an age when retirement becomes a possibility, it is necessary to know the position that the Age Pension plays in relation to superannuation and individual dependency savings. The 2026 update also projects the centuries-old trend of indexed increases instead of an entire system overhaul, which means that current pensioners will often be able to anticipate increased over time with steady increases, rather than a system shock.

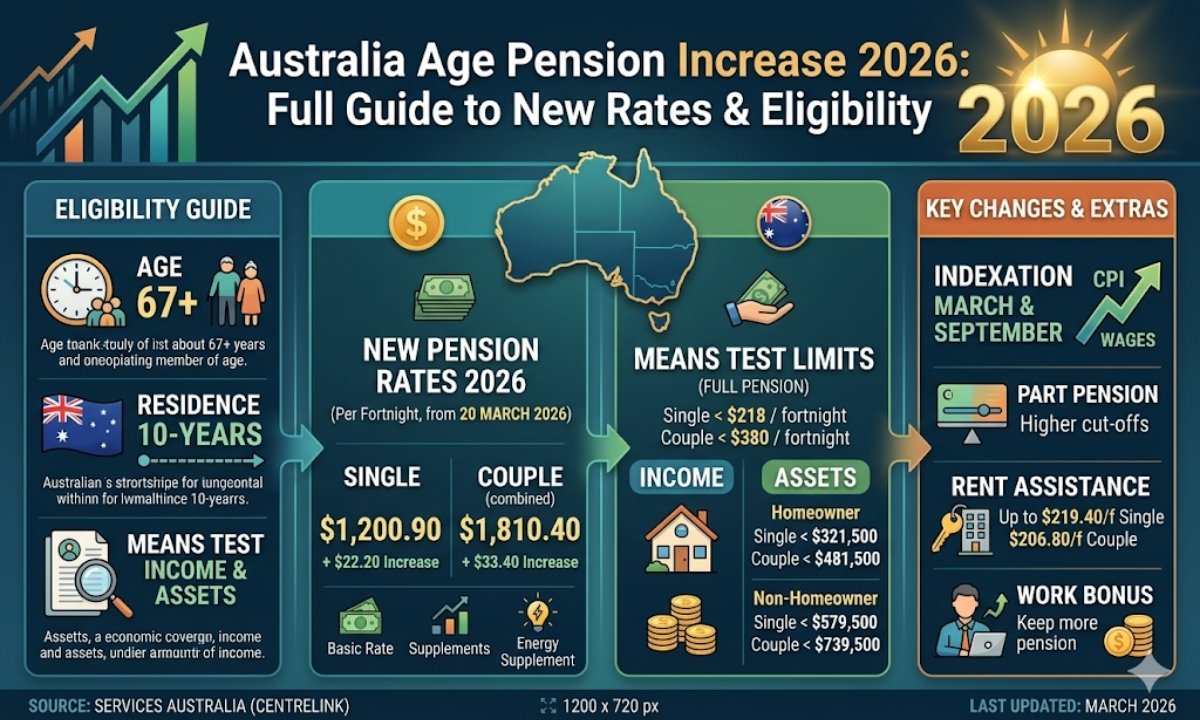

How Age Pension Rates Are Set

In Australia, the age Pension rates are usually adjusted after every six months, in accordance with the price movements and wages. The measure of a combination of indicators employed by the government to assist in ensuring the keeping of the terms of retirement by the pension in line with the reality about costs of life on the ground is a combination of Consumer Price Index and average wages. Practically, this implies that the amount of payments is likely to increase with time, despite the fact that the system framework may not be changing significantly.

The same indexation framework is taken in 2026 with the increase. Majority of the changes are percentage based but not flat one off bonuses. The maximum rate of single pensioners and couples is different as it represents the difference in the cost of living with one and two people. In addition to basic pension, several retirees also enjoy augmentations, like energy supplements, pension supplements and so forth, which can be adjusted jointly or distinctly.

New Rates at a Glance in 2026

To enable you get an idea of what an indexed increase would look like in a fairly normal year, the table below represents a hypothetical case only. These amounts are only illustrative and not the official government rates and always refer to Services Australia or government announcements on the exact current amounts.

| Recipient type | Example previous fortnightly rate (AUD) | Example 2026 increased rate (AUD) | Notes on change |

|---|---|---|---|

| Single | 1,100 | 1,140 | Standard indexation, modest real increase |

| Couple (each) | 830 | 860 | Paid to each eligible partner |

| Couple (combined) | 1,660 | 1,720 | Shows impact at household level |

In a normal indexation cycle, increment can appear meager on the paper but can have significant impact within an entire year when accumulated together with other concessions and supports. Predictability is the major concern of many retirees, and the 2026 target carries on the already begone pattern of increment by design, rule of thumb increase. When you are looking at the official data published, attempt to calculate your new rate of compensation against the amount of total income you had earned in the previous year so that it is easy to know the amount of additional assistance you are getting.

Who Can Qualify as a 2026 Rules.

The basic eligibility examination of the Age Pension further depends on age, residency, and means examination. To begin with, you need to be of the qualifying age that has been steadily rising and is currently set at later retirement ages as opposed to that of the older generations. Second, you should have spent a given number of years as a permanent resident in Australia with some exceptions being made in respect to persons under international social security agreements.

In addition to the age and the place of residence, the income and assets tests define the extent of what you can actually obtain. The government considers your assessable income, which is the income so far generated by investments, labor or other sources and the values of your assets, property (which in the vast majority of cases does not include the family home), savings and investments. In case the amount of money or assets you have earned exceeds a pre-determined limit, your pension will be dwindled or discontinued. The government keeps indexing these thresholds periodically in 2026 and this can make access a little more liberal or entitlements unaffected by the fact that the savings by people have increased in nominal terms.

Top Ten Useful Things to do to M.A.X. your entitlement.

In 2026, when you are close to the age (eligibility) it is time to begin by getting together the important documents, they include; provide evidence of your identity, residency details, superannuation accounts, bank accounts and holdings, as well as information about any investments you have made. Paying early before you reach your pension age, can assist in eliminating these gaps of not working a full-time and then getting your first payment. Online application made at Services Australia is typically faster, however, you may complete your application face-to-face or via phone in case you need a guided application.

Taking a second look at the effect of your superannuation withdrawals and part time work on your means tested payment is also prudent. Other retirees decide to change their approach and timing to investing profit to remain within the Age Pension limits without encountering their lifestyles. By talking to a licensed financial adviser or a free government financial counselling service, you can work out how to make the Age Pension supplement and not offset your other retirement income.

Anticipations: An Investment Horizon Longer Than 2026.

Although the Age Pension is set to rise to 2026, it is meant to be a safety-net, rather than a full substitute of a comfortable pre-retirement wage. The most viable and solid plan of retirement, to the greater majority of Australians, will be a mix of Age Pension, income streams of Superannuation and personal savings. In making multi-year budgets, it should be assumed that there will be indexation, but there is no need to rely on any big, one-off policy changes except when announced.

It is always best to review your retirement plan after every one or two years to keep you on course as rules, rates, and your circumstances change. Verify Age Pension rates, verify that you are eligible, and reduce your projections of incomes in the future. When the 2026 boost is viewed as a single step in a lifelong process rather than a one-temporary increase in wealth, you are in a stronger position to make knowledgeable and certain work, saving and lifestyle assumptions in retirement.

FAQs

Q1: What is the date of the 2026 rise of Age Pension?

It is usually applicable since the date of indexation declared by the Australian government in reason of that year; been Services Australia when the particular date is.

Q2: Will I be able to work and be receiving the Age Pension in 2026?

Yes, however, your salaries are counted under the income test, and thus more money in your pay (after passing the appropriate threshold) will decrease your compensation.

Q3: Is the home of the family a factor in the rate of my Age Pension?

Other properties and investments are also counted when determining your entitlement in general the principal home is not subject to the assets test.