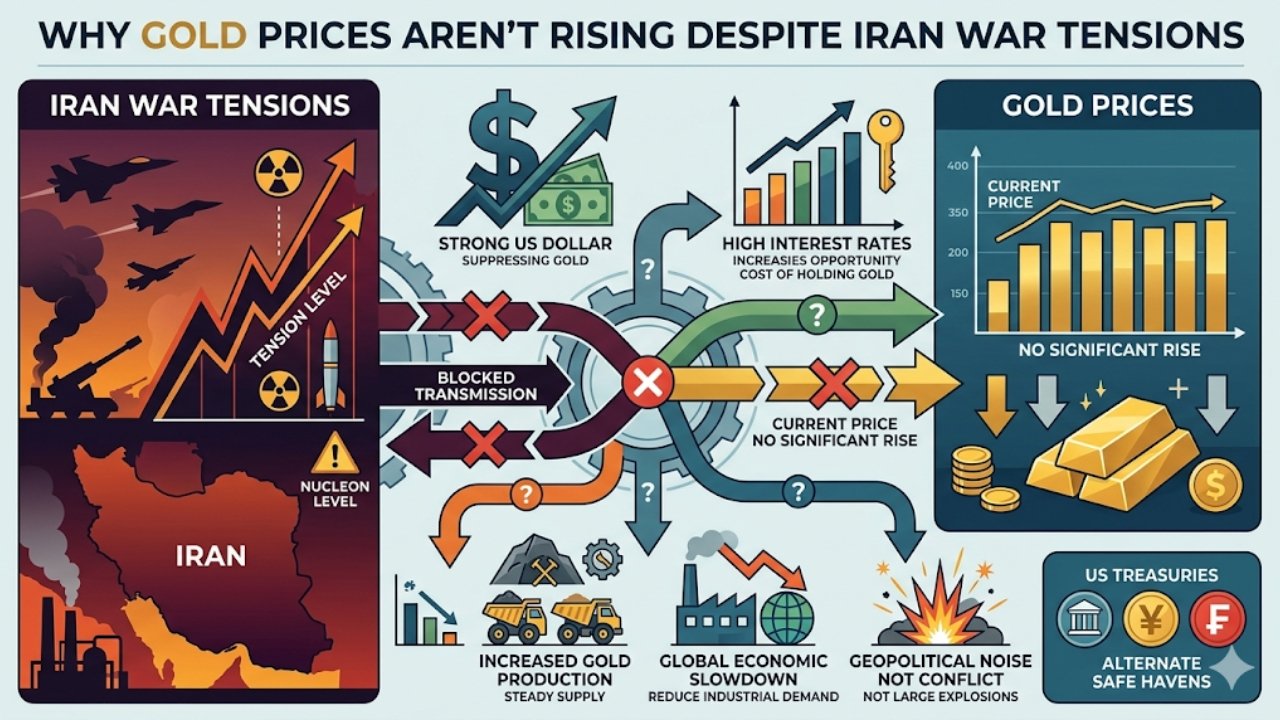

The prices of gold have been perceived as a safe-haven when there is a geopolitical crisis and hence most investors were surprised not to see the prices boost despite the escalating tensions surrounding an Iran related confrontation. However, rather than sharp rise, the bullion has traded flat or even given a slight slip back which leaves all traders and savers puzzled by the fact that the metal is not responding as it has been doing in the past. In order to see this deviation, it is best to move past headlines and consider the real-time motions that move the gold and stick to them more accurately than any one war or attack.

The manner in which gold normally responds to war.

This is actually historically true whereby gold increases when war or other serious conflicts erupt due to the high rate at which investors run towards assets that they consider safer than stocks or currencies. Wars shake political faith, strangled trading paths, which have been inflammatory, and the probability that the central banks will issue more money all of which generally favor high prices of gold. However, in the case of Iraq invading Kuwait in 1990 or as the Russia-Ukraine conflict erupted in 2022, such as with gold, then that gold initially jumped on the uncertainty protection buy by investors.

But such moves are not often mechanical. Occasionally the bump is small, occasionally it is temporary, and occasionally markets put their heads in the sand and forget about the conflict. The market is once more considering the risk, this time, with a very different backdrop of interest rates, bond yields, and expectations of monetary policy, due to the existing Iran related tensions.

The reason why Iran tensions are insufficient in their own own.

Many investors are currently considering the war-relating Iran as the risk-on, yet limited scenario in 2026, instead of an actual war that would encompass regions. There are some tangible reasons as to that. To begin with, the asset prices have already been adjusted to existent sanctions and military placements that have taken place in the last couple of years, meaning that new headlines are no longer that shocking as they could have been previously. Second, the dispute has remained so far below the level of a full-blown war that would block key oil-transmitting routes or engage one of the world superpowers in combat.

Safe haven effect on gold is likely to be dampened when no disruption to supply chain or energy flows is immediate and of a large scale when observed in the markets. Rather, the focus of what traders are concerned with is the behavior of the central banks, energy markets, and currencies. In the event of a only moderately increasing oil prices and bond yields, which remain in the range, gold will be able to easily lag even during anxious headlines.

The interest rates and bond yield.

Among the many factors which have made gold not take off is the fact that cash like assets are becoming better due to the increasing interest rates and the relatively stable bond yields. Gold is not interest-bearing and in this instance at rates of high interest when inflation is not running out of control, investors would oftentimes choose to have a short-run Treasuries or money-market funds rather than storing their money in bullion.

There are also a number of key central banks that have maintained the policy rates at levels that make the opportunity cost of keeping gold levels relatively high in 2026 such as the U.S. Federal Reserve. Meanwhile, the bond market has not deteriorated into a full-scale fear spiral, thus, causing long-term yields to fall and gold to soar. With a yield curve that stays approximately constant, models that stay in a range are still valid even in the case of geopolitical noise.

An overview of the recent environment of gold.

To elaborate on this, table below shows some of the main indicators that can help in explaining why gold is not soaring even with the Iran related tensions.

| Factor | Current situation (2026) | Effect on gold price |

|---|---|---|

| Policy interest rates | Still elevated in major economies (U.S., Europe) | Weighs on gold |

| Inflation | Moderating, but not falling sharply | Neutral to mild support |

| Geopolitical risk (Iran) | Elevated, but no full‑scale war yet | Mild support |

| Bond yields (10‑year U.S.) | Stable within a defined range | Limits gold upside |

| U.S. dollar | Firm or slightly stronger | Puts downward pressure on gold |

| Physical demand (India, China) | Healthy, but not surging to record levels | Mixed, modest support |

Such a combination of circumstances does not imply that the classical war-scares-push-gold-up script is not running smoothly. Rather, investors are balancing the possibility of a localized war against a regional one and have been leaning towards the former as yet.

The implication of this to investors is as follows.

To individuals possessing gold in their portfolios, somehow in the form of coins, and ETFs, or even digital options, this environment proposes some of the following. First, gold did not become useless as a hedge although it is not sure that it will spike every time on a headline. Second, it is risky to implement short-term decisions grounded on the news of political implications and geopolitics only since the metal might remain flat or even declining when the trends in the interest rate and currency dominate.

A fairer solution here is to consider golden as a diversifier to be used as long-term to ease into an inflation or unforeseen crisis as opposed to acting as a quick-trade when new fights or attacks become headlines. In the case of conservative investors, a small amount of investment in gold and observing fluctuations in interest rates and currency may provide them with a viable compromise.

FAQs

Q1: Why not gold is going up when there is a war in Iran involved areas?

Not only the presence of tension but also the perceived size and length of conflict make Gold react. In case the markets perceive the Iran related scenario as capped or already anticipated and interest rates are high and the dollar strong, gold may stay flat and even could be on the decline despite the headlines.

Q2: Certainly, gold is always a winner in wars or other conflict situations?

No. Gold tends to appreciate in large wars or crises but the trend may be slight or temporary on the event that the conflict remains constrained, inflation rate low or maybe because increased interest rates can make alternative assets to be preferable.

Q3: What should I do with gold in my investment?

Gold should be used as a long-term diversifier, but not as a speculative bet about all the geopolitical events. Compared to an overweight investment, a small portfolio will keep you out of inflation and any other sudden shock, although you need a clear picture of interest-rate and currency trends.