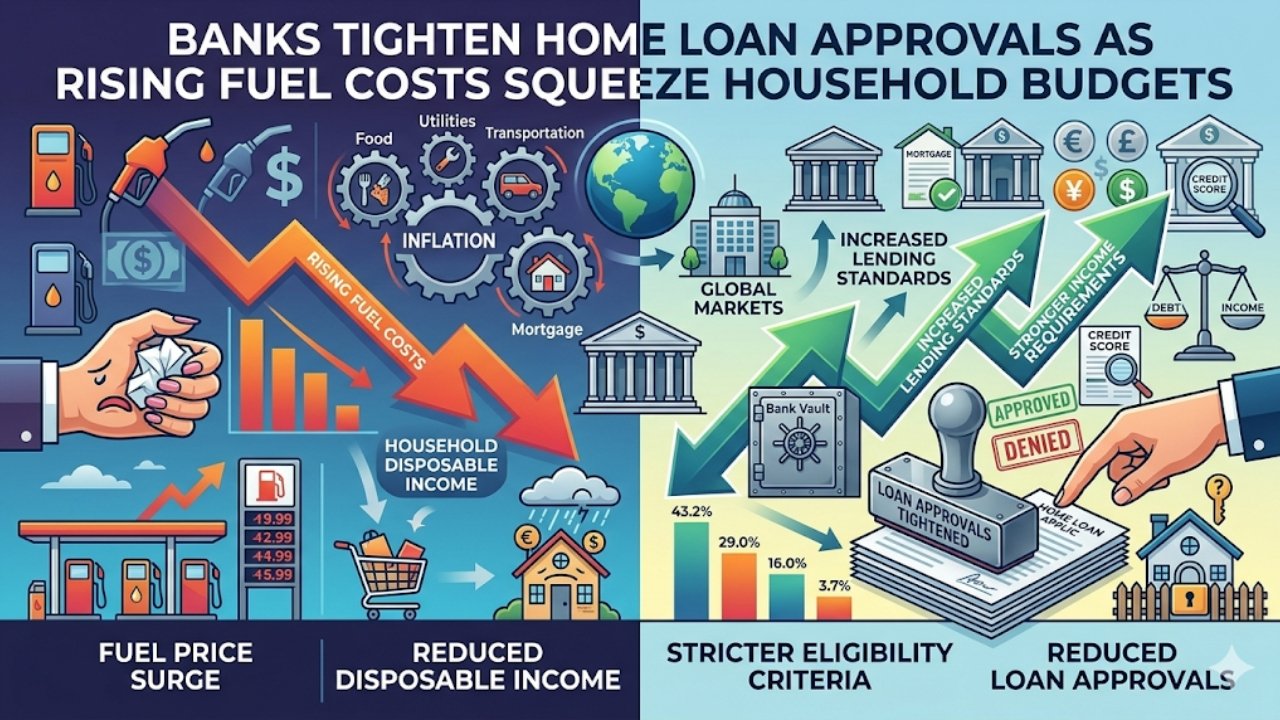

The homeownership dreams are also experiencing downturns in India with the banks limiting loan advances. The price of petrol and diesel is also gradually increasing to a high of 105 per liter in big cities like Chandigarh and Delhi, thus making budgets run tight. Families who combine EMIs and groceries with gasoline debts increase their debt to earnings ratios and creditors are being stricter. Data on housing loan disbursals at Reserve Bank of India in early 2026 supports this trend by showing a 12 per cent reduction in the disbursals when compared to the previous quarter, indicating to be on a negative trajectory with economic headwinds.

The fuel expenses that have increased 15 per cent annually owing to the volatility of oil prices in the global market and the depreciation of the rupee are a tax in disguise to the daily living. In Chandigarh, an average middle class commuter gets to incur an additional 3000 a month on fuel than he or she did last year, and the money would have been saved to down payment. Banks which on norms of the RBI are now far stricter on quality of assets are now examining their applicant better. A credit rating of below 750 will result in out anright rejection and the strong profile will also experience calls of increased income or collateral. This restriction is a cautious reaction to an increase in non-performing assets in retail loans, which increased by 2.5 per cent in the recent Financial stability report.

A vicious cycle of the Fuel-Household Squeeze.

Having a fuel price that is soaring affects in all the areas of the finances of the household making it a cost breaker. This means that in the case of an urbanite worker who commutes to his or her place of work using 50-60dm per day, the calculation will be ruthless: a 10-litre tank-up will take in 1050 INR today, but it took 900 INR half a year ago. This compels trade-offs in other areas such as eating out less, hold off on upgrading your car or even holding off on buying the house that you so wanted.

Worse still, core inflation is spurred by inflation in transportation fuel, which increases the prices of all products such as vegetables carried by trucks to the Punjab farms to online products. According to one recent Nielsen survey, households say they would cut discretionary spending by a fifth, but fixed expenditures such as rent and education loans are not going down. When determining eligibility, the banks consider these realities through the debt service ratios (DSR) when it is more than 5060% of take home salary, it concentrates approvals dry up. In Chandigarh, where the real estate is riding on the new IT hubs, the potential buyers in other sectors, such as the tech and manufacturing industry, are the ones who are at the receiving end of the pinch, since the variable bonuses will no longer impress lenders.

How Banks Are Transforming the Game.

Lenders are not simply turning no, they are simply redefining the terms and conditions. The HDFC and SBI, both giants in home finance, have increased interest charges by 0.25 0.5 percent on floating loans as early as January 2026 citing the increases in the repo rate to counter the inflation. Turnaround time is extended to 45 days instead of 30 and further documentation is required: three months bank statements, 2-year ITR, and even utility bills to check on address stability.

Computerized underwriting systems are currently red flagging high fuel sensitive areas, and comparing the applicant pin codes with the oil price indices. On the part of salaried borrowers, they experience an increase of 10 0% in the minimum income to cover the pressure of cost of living. It is even harder on self-employed people who require 25 per cent of additional turnover evidence. This warning is based on the experience of the 2020 pandemic, when fuel shocks increased the number of defaults a decision banks will never repeat.

Factors: Trend of Home Loans on the rise against fuel surge.

In comparison, to demonstrate the effect, here is the snapshot of housing loan metrics of RBI and CRISIL data within Q4 -25 to Q1 -2026:

| Metric | Q4 2025 | Q1 2026 | Change |

|---|---|---|---|

| Total Disbursals (₹ Cr) | 1,20,000 | 1,05,600 | -12% |

| Rejection Rate | 18% | 28% | +10 pts |

| Avg. Loan Size (₹ Lacs) | 45 | 42 | -7% |

| Delinquency Rate | 1.8% | 2.3% | +0.5 pts |

The following table underlines how tighter lending and smaller tickets can be associated with fuel-related squeezer in an attempt to allow borrowers to compare their condition.

Buyers Strategies to Go through the Crunch.

Would-be house owners can not weather the storm, prudent actions now can get the go-ahead. The first move is to create a six-month emergency fund (fuel and necessities) and aggressively accumulate debt to reduce your DSR to 40 and lower. Choose co-applicants such as spouses to increase income, provide affordable suburbia in the Mohali extension of Chandigarh where EMIs would be within budget ranges.

Replace the current consumption with fuel efficient hybrids and save 1,500 every month to pay off the current bills in advance thus enabling better credit histories. Government programs such as the Credit Linked Subsidy of the PMAY are still life aquifers to first-timbers, receiving a discount of 3-6.5 per cent – however, take sooner before the quotas are filled quickly. Lastly, price hunt: It may also be worth looking at NBFCs such as Bajaj Finserv, which can have more relaxed conditions than the banks, at a higher price though. Timing is also important – wait until April 2026 when the next policy review is done and rate cuts would relieve pressures by RBI.

Opposing Side: Is Reprieve in Sight?

The only possible solution is that the fuel costs will be stabilized when OPEC+ increases production or the rupee recovers, yet the banks will not be quite convinced unless the NPAs begin to peak. In the short term, this squeeze theorizes away over-levered purchasers, which makes the market healthier in the long run. It should be seen as a call to strengthen finances rather than throwing off the goals by aspiring owners in Chandigarh and farther. Your dream house is in your reach with a disciplined planning.

FAQs

Q: What reasons are banks giving nowadays in rejecting more home loans?

A: Inflation and increased fuel cost decreases the ability of repayment, and debt ratios are further too high per the RBI guidelines.

Q: What is the effect of additional fuel cost on the loan eligibility?

A: An additional 2,000-4,000 a month would bring DSR up by 5-10% percent which regularly swings approvals to rejection.

Q: How can loans be increased in a better way?

A: Pay down debt, save, and include co-applicants to enhance your earnings.