The capital gains tax rate is reduced on capital gains that the investor has invested in an asset with at least one-year holding period in an attempt to make investors invest long-term. In Australia, e.g., the discount is reduced by half and made 50 -percent to individuals as a reward to bide time, rather than to make and break a bet. With governments facing an increase in debt and an aging workforce, according to critics the benefit puts an additional burden on the young generation by imposing more taxes in other areas.

Causes and Intention of the Discount.

Capital gains discounts were introduced by policymakers many decades ago so as to spur economic growth. The idea of taxing only a half of the increase on marginal rates was made to make saving and investing more appealing than spending or pure speculation business. This was a transition to accumulate wealth across the society to finance retirements, as well as businesses but not to deter the risk.

As a matter of fact, the playing field is leveled between wages, which are taxed and taxable immediately, and returns in investment made over time, which come with inflation and risk. Advocates cite soaring stock markets and housing markets as evidence of its success, and its assets in trillions are currently receiving this kind treatment. In their absence, they claim, the capital would be shifted to other lower tax jurisdictions and they will lack the necessary cash to fund their economy.

How It Works in Real Terms

Take an example of an investor who sells his stock purchased at price 100,000 which has increased to 200,000 after two years. The gain will only be taxed at 50 per cent, so savings in higher rates could save thousands of dollars. This is the case with shares, property and other assets but primary homes or small-business exception are available.

The assumption behind the policy is that the long-term holdings are in accord with societal good like stable companies generating employment. It has been recorded that average effective rates declined to less than 20 0 -percent of many, much lower than the rates paid to income-tax payers on its daily wages. This is what governments boast as equitable payment of uncertainty that investors undertake.

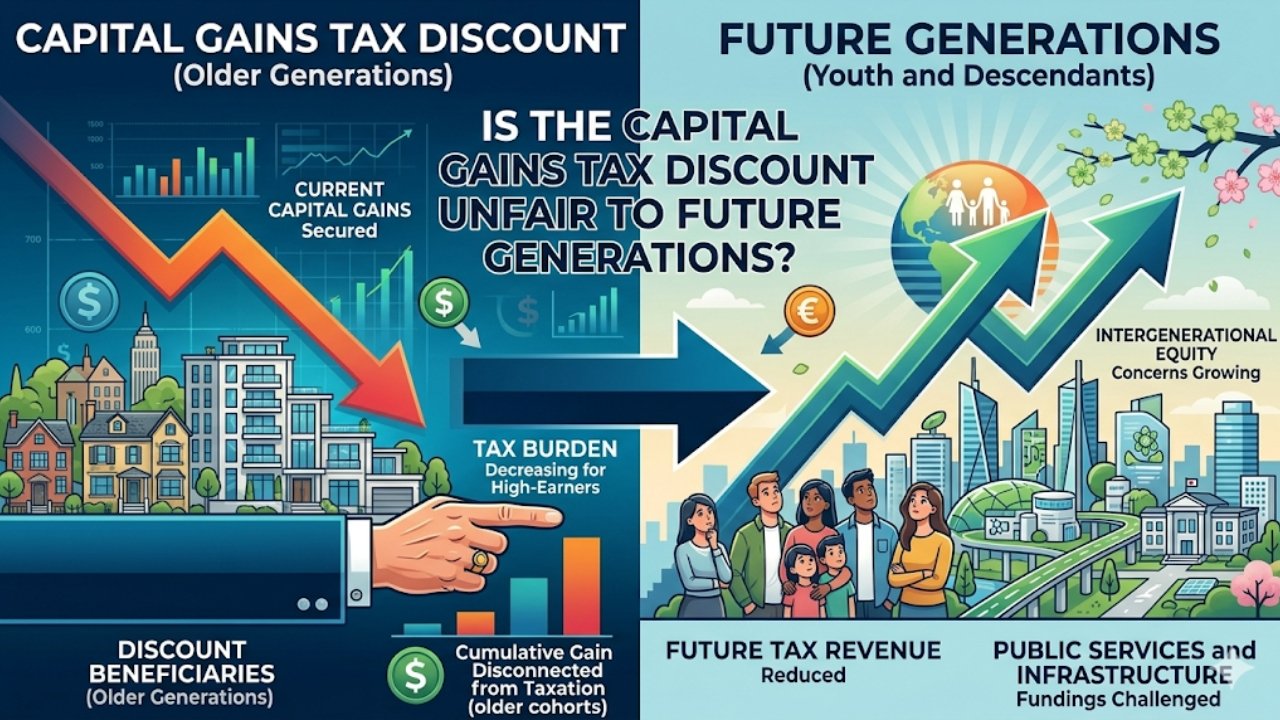

Brunt on Generations to Come.

Here fairness cracks. Younger generation members, with student debt and growing stagnant wages, watch their superannuation funds bloat tax free or discounted to boomers swamped with cash. The amount of revenue that is lost, which is estimated to be in billions per year, translates into increased taxes on income or consumption to take up shortfall, adversely affecting those of working age.

This puts pressure on public services. Pie is watered by needs like roads, schools and healthcare at time when capital gains discount can reduce the size of the pie. With aging populations, pension claims are going out of control, and the burden on the taxpayers of the future has to be increased further, with the risk of receiving overvalued asset prices that were in part caused by tax-favored investing.

Aspect Current Impact Future Generation Effect.

| Aspect | Current Impact | Future Generation Effect |

|---|---|---|

| Revenue Loss (Annual) | $20-30B (e.g., Australia) | Higher income taxes (+2-5%) |

| Wealth Distribution | Top 10% hold 80% gains | Reduced inheritance mobility |

| Debt Servicing | Lowers gov’t borrowing capacity | Increased national debt share |

| Asset Price Inflation | Boosts housing/stocks 15-20% | Harder home ownership |

This table reflects some of the important imbalances, based on fiscal reports in the discernment of countries accounting to the discounts.

Economist Counterarguments.

Proponents of defender nullify this by arguing that scratching the discount assassinates incentives, decelerating growth favorable to everyone. Research correlates the low level of capital taxation with elevated GDP per capita where investments pass through jobs and creativity. Even though there might be increased taxation in other areas in the present, they say, the future generations benefit because they have a richer economy.

Gradual withdrawal will invite capital flight – imagine rich pensioners to tax havens. Also, inflation destroys returns in the long run; taxing of full amounts does not take into consideration this fact. Such reforms as means-testing or discount capping solve inequities without destroying the system keeping long-term incentives.

Striking a Balance between Fairness and Growth.

The policymakers have to make a trade Off between intergenerational equity and dynamism. Tweaks redistributing the discount to 30 per cent or to income levels would be able to claim back revenue without chilling markets. A combination of this and superannuation caps will make sure that the retirees do not amass benefits that are not reasonable.

Finally, the discount is not necessarily unfair, it is a trade-off device. Future-proofing requires transparency model scenarios of how adjustments would have an impact on growth, debt, and mobility. Voters should get serious arguments, not soundbites.

Paths Forward for Reform

Specific changes are the most light. Discounts should not only be extended on productive assets, such as the business equity, but not passive rentals which contribute to the housing crises. Appendix able to incorporate claw-back on estates that exceed the net worth, obtaining proceeds on inheritance. These maintain incentives and repackage gains.

Countries that are not having discounts such as in some parts of Europe experience mixed outcomes. Hybrids become victors, who combine development with unity.

FAQs

Q1: What was behind the capital gains discount?

Implemented during 1980s-90s in order to stimulate recession investment.

Q2: Does it really save billions?

Yes, lost income goes up to tens of billions each year in the largest economies.

Q3: Can it be reformed fairly?

Yes, it is the balance of incentives and equity is provided by means-testing and caps.