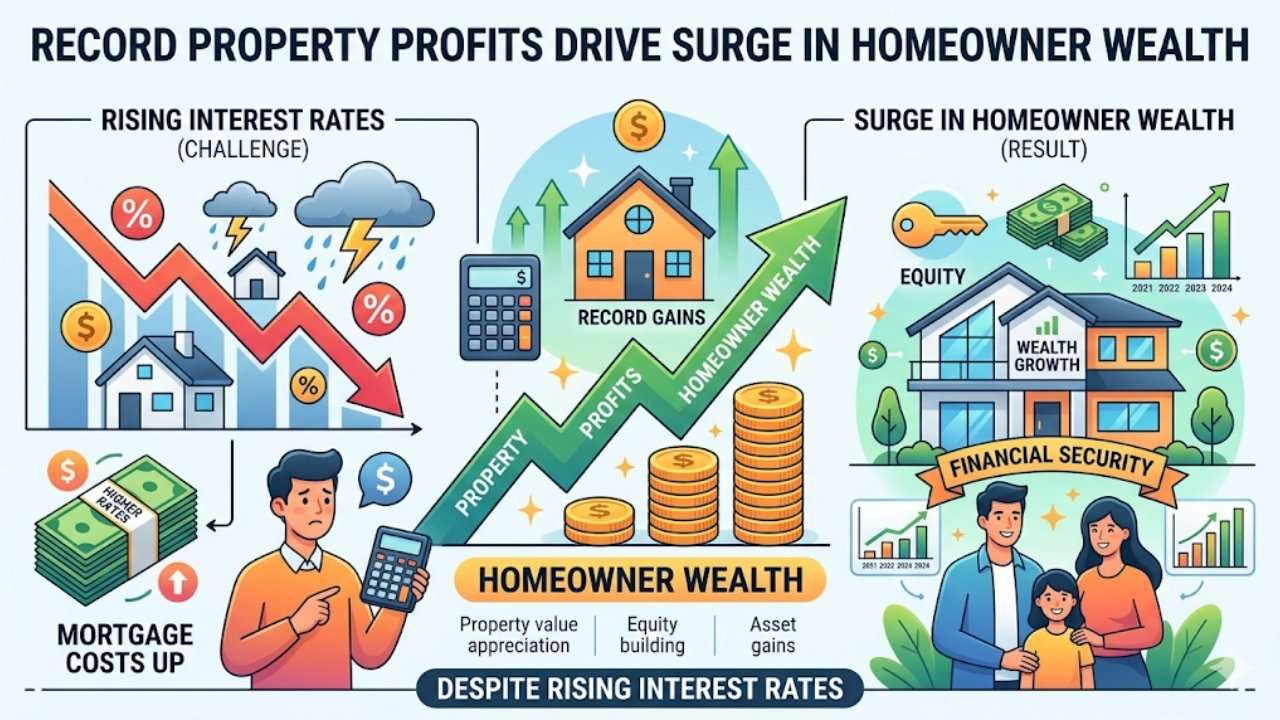

In the world, homeowners are enjoying the growth of wealth like never before. The primary impetus is the soaring property values, although the central banks maintain the interest rates high. Stunningly, residential real-estate equity will reach a mind-blowing market figure, 32 trillion, by the end of 2025, Federal Reserve records indicate, in the United States alone. The increase of that percentage is 10 per cent as compared to the last year. This growth remains in the face of benchmark rates of about 5–6 per cent in the leading economies of the west such as U.S., U.K and some European regions. They have families that purchased houses ten years ago and now have their net worth inflated, their decent investments transformed into game changers. What is the reason why this resilience survives? The shrewd house owners are taking advantage of locked up low-rate mortgages during the pandemic that protect them against the current high mortgage rates as land values skyrocket much faster than inflation.

There are several steps involved in unpacking the Property Profit Engine.

The boom is precipitated by brute mathematics: houses continue to increase in value at a faster rate than most other investments. Migration into cities, low housing construction and post-pandemic demand to have bigger living spaces have resulted in an increase of 45 percent of median home prices over the past two years in major markets. Consider Austin, Texas or Manchester, UK – they both experienced a higher appreciation of over 8 per cent/year in 2025. A cash-in by homeowners occurs in the form of equity extraction (Home-equity line of credit (HELOC)) which allows them to borrow at rates that are usually cheaper than personal loans against accrued or built-up value. This plan avoids the expensive mortgage rates that new purchasers have to pay which go at 7 percent or above on 30-year fixed mortgage. The result? Along with financing renovations or building their wealth by investing in stocks without selling, they add to retirement funds through existing owners.

Scamming the High Rates: What to do.

An increase in rates, which is used to tackle the slow inflation rate, puts pressure on new entrants but has little effect on those who are established. The people who pegged mortgages at foregone rates below 4 percent in 20202022 would not sell to restrict supply and support the price. According to Redfin data, in 2020, year-over-year rate-locked sellers declined by 30 per cent, and this left the sellers with a market. House owners who employ services of Smart Home rent out parts of their houses on Airbnb, thus earning a passive income that serves to counter rate increase in variable debts. This is demonstrated by the case of urban home owners in such cities as Chandigarh in India where a 6.5 per cent repo rate gives them 12-15 per cent value growth, which is combined with rental yields to give a healthy returns.

Important Statistics: Home Equity Increase vs. Rate Trend.

As an example of how unrelated rates and wealth have become, the following snapshot of U.S. trends in 2023–25 (based on Federal Reserve and NAR reports) will illustrate the point:

| Year | Avg. 30-Year Mortgage Rate | Total Home Equity (Trillions USD) | YoY Equity Growth |

|---|---|---|---|

| 2023 | 6.8% | $28.5 | +7% |

| 2024 | 6.2% | $29.8 | +5% |

| 2025 | 5.9% | $32.0 | +7% |

The following table shows a gradual increase in the equity even at peak rates, and this indicates the importance of property as an inflation hedge.

Greater Economic Spillovers and Future risks.

The prosperity wave extends and enhances consumer expenditure and stabilising economies. According to LendingTree, U.S. homeowners borrowed $500 billion against their home equity last year on all items such as home improvements to debt refinancing. Yet cracks loom. At current rates, millennials and Gen Z affordability can plummet in 2026, increasing inequality. Canadian overheated Toronto market is one of the regional bubbles. Moody analysts forecasts 4-6percent growth that is moderated in 2026 and recommends that it should be diversified. Nevertheless, to the 70 million U.S. homeowners, it is their real-estate that quintessentially makes them the wealth-creator, surpassing unpredictable stocks or bonds.

Moving on: Continuing the Momentum.

With the world economies contemplating a reduction of the rates before mid-2026, house gains will gain momentum but the current owners are already on top. The proactive policies, such as energy-saving renovations that are tax deductible, or joint purchase with family members, will maximise benefits. It can be found in areas such as Chandigarh, India, where infrastructure booms have the purpose of creating 10 percent or more increases, local experience is paying off: developers report a green home premium in urbanization. This wave is ultimately the long-run significance of real-estate and it pays off during a rate storm.

FAQs

Q: Why is property value trending high regardless of the high rates?

A: Prices keep rising due to limited supply of sellers who are locked into the rate and great demand.

Q: Can this trend be applied to the benefit of renters?

A: Yes, shared equity plans or saving down payments in those and/or up and coming regions.

Q: How do you now optimally tap home equity?

A: HELOCs are to be used to borrow in low rates, but should be considered with a financial advisor.